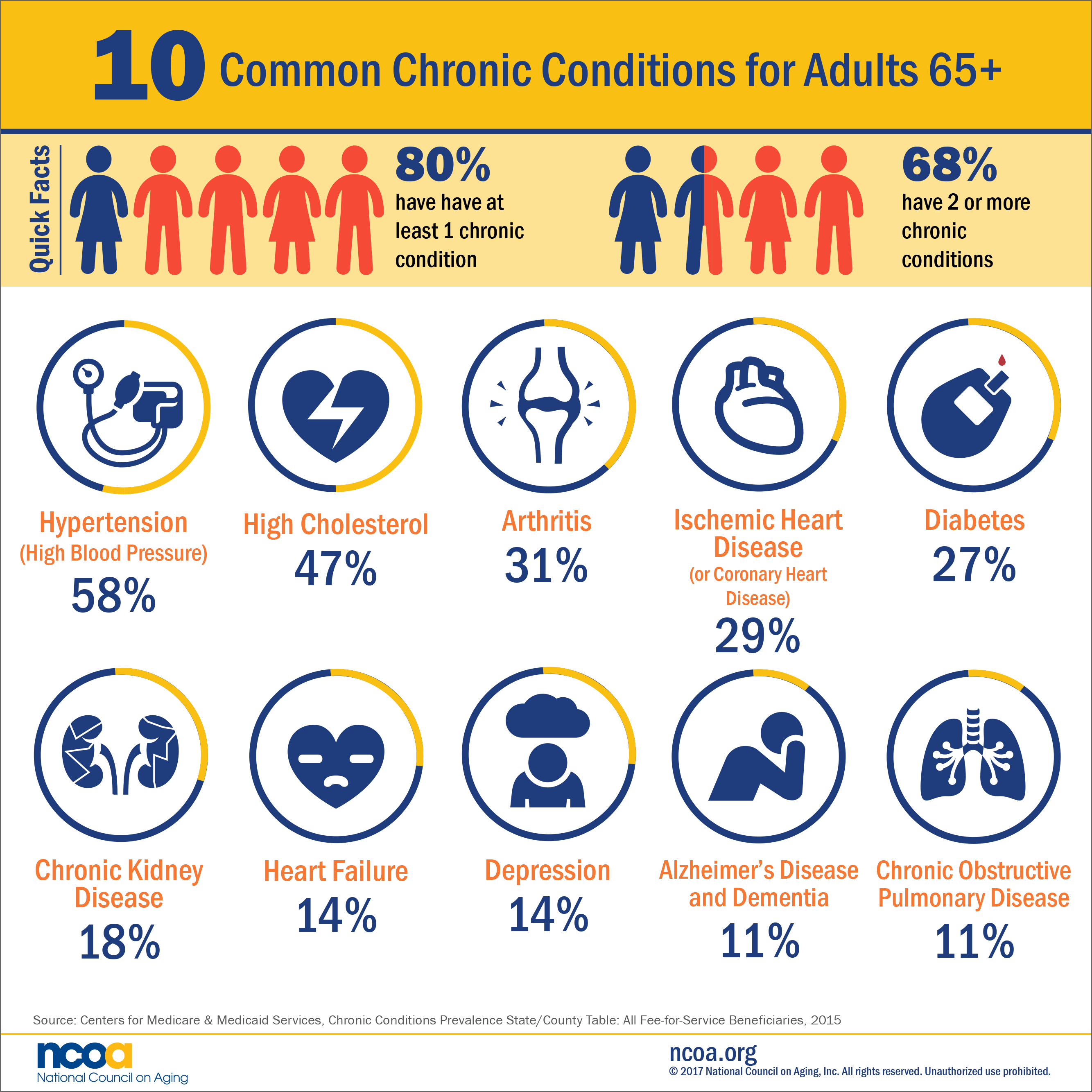

It’s difficult to understate the importance of planning for long term care expenses later in life. According to the National Council on Aging, 80% of adults age 65+ have at least one chronic condition, and 68% have two or more chronic conditions.

Long term care is not covered by Medicare or traditional health insurance plans, so the expenses associated with these conditions can quickly eat up your savings if you’re not prepared. And unfortunately, Medicaid will only help you pay for long term care after you prove that you have already spent down virtually all of your assets.

Due to the financial risks associated with long term care, it would seem that long term care insurance should be a crucial element of any retirement plan.

However, many potential buyers are wary of LTC plans due to the widely publicized drawbacks of the traditional LTC insurance industry, such as volatile premium increases and companies losing millions of dollars due to miscalculations associated with these plans.

Another weakness of traditional LTC plans is the “use it or lose it” dynamic of the LTC benefits. As a policyholder, if you never need to use the LTC benefits, you never receive anything from the policy. It can be difficult to justify paying a high annual premium (that may be subject to an increase at the insurance company’s whim) for a plan that you may not receive any financial benefits from.

If you need coverage but are wary of purchasing a traditional LTC plan, here are some common alternatives to long term care insurance:

Self-fund

You can pay for long term care out of pocket if you have enough savings. However, it can be difficult to predict how expensive your care will be, since so much of it depends on the kind of condition you have and the level of care you need.

Life insurance with chronic illness benefits

Some life insurance policies – both term and permanent – include chronic illness benefits, which function in much the same way as long term care benefits on an LTC policy.

These are sometimes called ‘living benefits,’ and in order to qualify to receive benefits, a doctor must certify that you have a condition that prevents you from being able to independently perform at least 2 of 6 Activities of Daily Living: eating, bathing, toileting, dressing, continence and transferring. Severe cognitive impairment is also covered.

The advantage of securing chronic illness benefits on a life insurance policy vs. a traditional LTC policy is that the product is priced and underwritten as a life insurance policy rather than a long term care insurance policy. You can get coverage without having to worry about the volatile premium increases associated with traditional LTC products, and many life insurance products even offer a premium guarantee that is built into the policy.

Another advantage is the benefit payout. Some of these policies offer an indemnity payout option, which means that once you qualify for the chronic illness benefits, you receive the annual lump sum directly and decide for yourself how to use the money.

Traditional LTC plans, by contrast, use a reimbursement model, which requires you to only receive care from approved caregivers and submit receipts to the insurance company for reimbursement.

Hybrid long term care insurance – Single premium

Hybrid LTC plans are life insurance policies that usually offer more robust long term care coverage than the ‘chronic illness’ plans mentioned above.

These plans are ideally funded with a large single premium payment ($100,000, for example). However, they can also be funded in annual installments spread out over a period of 5-15 years.

A popular way to help fund hybrid LTC plans is to use a 1035 exchange to transfer cash value from an existing life insurance policy into a hybrid policy that includes long term care benefits. The exchange is tax-free, making this an ideal way to fund a new policy.

Due to the large financial commitment required to fund a hybrid policy, many plans come with full or vested 'return of premium' options, which allow you to receive a refund of your premium should your plans change.

Hybrid LTC plans offer more security than traditional LTC plans because they provide guaranteed LTC benefit amounts for the premium you are paying. You know what you’re getting and you don’t have to worry about the insurance company increasing your premium.

And if you never need to use the long term care benefits, your beneficiary will receive a full death benefit from the policy. This means that no matter what happens in your life, the policy will provide value.

LTC annuity

Some annuity products include long term care riders.

The advantage of the LTC annuity is that the underwriting is not as stringent as a traditonal LTC or hybrid life/LTC product. If you have health conditions that may create underwriting problems with other types of products, an LTC annuity can be a great option.

Like the hybrid life/LTC products mentioned above, LTC annuities require a large upfront payment (for some products, the minimum is $50,000).

If you don’t need to use the LTC benefits, it is possible to redeem the annuity’s accumulated value.

Deferred annuity

A deferred annuity can be used to plan for potential LTC expenses in retirement. For example, a 55 year old man can take out a deferred annuity that will start distributing monthly payments when he reaches a certain age (72 for a qualified retirement account).

The difference between a deferred annuity and an LTC annuity is that the monthly payments are not specifically allocated for long term care, and it does not cover any long term care expenses incurred before retirement.

Immediate annuity

An immediate annuity provides immediate monthly payments in exchange for a large upfront single premium.

The advantage of this option is that you can obtain monthly payments to pay for long term care even if you are in poor health and cannot qualify for other types of products.

However, the monthly payments may not be enough to cover your long term care expenses, especially if you require skilled care in a nursing home. The amount of monthly payment will depend on your premium amount, age, gender and overall health.

The tax implications can be complex, so you should consult with a knowledgeable agent or tax advisor.

Conclusion

Ultimately, the best course of action is to plan ahead rather than wait until you are almost at the age when you might need coverage. There are many alternatives to long term care insurance, but age is usually one of the most important factors in determining what kind of value you will get from these products.

Whether you're considering a hybrid LTC policy, a 'chronic illness rider' life insurance policy, or an LTC annuity, it helps to apply when you're young and in good health. The ideal age to apply for a hybrid policy is in the 50s to mid-60s.

Many of these policies include inflation riders that allow the pool of LTC benefits to grow over time, so the younger you are when you apply, the more time you have to let the benefits grow in the policy.

COVID-19 Update: Several companies have temporarily limited the availability of their products to exclude applicants over the age of 70 due to the COVID-19 pandemic. We hope that this trend will not continue, and it illustrates the importance of planning ahead.

At Hybrid Policy Advisor, we provide guidance and quote comparisons for people who are looking for long term care solutions. We can help you find the solutions that are best for you and your family.

If you would like to learn more, give us a call at 1-866-365-6558, or click the button below to submit a quote request.

We look forward to hearing from you.